Suppose that I toss a fair coin, and offer you Rs 10 for a head,

and demand $Rs 20$ for a tail. In other words, your gain (in Rs)

from this deal is $10$ for head and $-20$ for

tail. Both $10$ and $-20$ are constants, but since you

do not know which of these two constants you are going to get,

you gain is a variable. Since it varies with chance, we call it

a random variable.

Think of this as made of two stages. In the first stage we have a random

experiment with $\Omega = $

{Head, Tail}. In the second stage we have a function

$X:\Omega\rightarrow {\mathbb R}$

defined as

$$\begin{eqnarray*}

X(head) & = & 10,\\

X(tail) & = & -20.

\end{eqnarray*}$$

There is nothing random about this function. The randomness comes

from the mechanism that decides what goes into this: head or tail?

We use this idea to define random variables mathematically. We

start with a random experiment which is the provider of the

randomness. Then any (real valued) function defined on its sample space is

called a random variable. In probability theory, it is the function

(which is not at all random) that is called the random

variable. Thus, if in the above coin toss example, we replace the

fair coin with a biased coin, but keep the payment rules the

same, then we still have the same random variable.

Beginners often find it odd: a random variable is neither random

nor a variable!

However, it is not as unnatural as it sounds. In calculus also we

write $y = x^2$ and say $y$ is a variable as well

as $y$ is a function of $x.$

EXAMPLE 1:

In the coin tossing example with a fair coin, let your gain be

denoted by $X.$ (or sometimes $X(w)$, if you want to emphasize

that it is a function). Find $P(X=10).$

SOLUTION:

The immediate answer is $\frac 12.$ Let's see the steps that led

to this answer. $P(X=10)$ is the probability that $X$

is $10,$ i.e., the probability that the coin toss has

produced an outcome for which the function $X$ takes the

value $10.$ Thus

$$

P(X=10) = P\big\{w\in\{head,tail\}~:~X(w)=10\big\}.

$$

Now $\big\{w\in\{head,tail\}~:~X(w)=10\big\} = \{head\},$ and so

the problem now reduces to finding $P(\{head\}),$ which is $\frac 12.$

■

The general case, then, looks like this: We have a random

experiment with sample space $\Omega.$ A random

variable $X$ is a function $X:\Omega\rightarrow {\mathbb R}$

where ${\mathbb R}$ is any codomain of our choice. If some one gives

us some $A\subseteq {\mathbb R}$ and asks us to find $P(X\in A),$ we

are to actually find

$$

P\big(\big\{w\in\Omega~:~X(w)\in A\big\}\big).

$$

Remember that this is the definition of $P(X\in A).$

The complicated looking set $\big\{w\in\Omega~:~X(w)\in A\big\}$ is

often abbreviated to $\{X\in A\}$ or $X ^{-1} (A).$

Don't let the notation $X ^{-1}$ make you think that $X:\Omega\rightarrow{\mathbb R}$ has to be

invertible. For any $f:A\rightarrow B$ we can define $f ^{-1}:\pow(B)\rightarrow\pow(A)$ as follows (here $\pow$ denotes

power set, i.e., the set of all subsets):

for $V\in\pow(B)$ we define $f ^{-1}(V)=\{a\in A~:~f(a)\in V\}$.

Sometimes we need to combine the values of two or more random

variables. Say $X,Y$ are both random variables and we want

to compute $X+Y.$ Since random variables are actually

functions, so this sum can be formed only when $X$

and $Y$ have the same domain. This simple point sometimes

needs careful handling as the following example shows.

EXAMPLE 2:

I am playing against two gamblers simultaneosly. One gambler

tosses a fair coin and pays Rs 10 for a head and takes Rs 20 for a

tail. The other gambler takes Rs 3 from me, rolls a fair die and pays me as many

rupees as the outcome. What is my total gain?

SOLUTION:

If I call the gain

from the first gambler $X,$ then $X$ is a function

from $\{head,tail\}$ to ${\mathbb R},$ while the gain from the

second gambler is a function $Y:\{1,2,3,4,5,6\}\rightarrow{\mathbb R}.$

Obviously, $X+Y$ does not make any sense here. We need to

first combine the two random experiments to get the product

sample space: $\{head,tail\}\times\{1,2,3,4,5,6\}$ and then

consider $X,Y$ both as functions from $\Omega$

to ${\mathbb R}.$ For example, $X(head,4) = 10$

and $Y(head,4) = 4-3 = 1.$

Now it is meaningful to talk about $X+Y.$

■

Is any function of a random variable is again a random

variable? Well, for if our $\Omega$ is a countable set (finite/infinite), then

the answer is "yes". We shall not worry about the uncountable case here.

EXAMPLE 3:

A fair die is rolled. I shall pay you Rs 10 if the die shows an

even number, you'll pay me Rs 20 otherwise. Let's denote

by $Y$ your gain (in Rs). Express $Y$ as a function from $\{1,2,3,4,5,6\}$ to ${\mathbb R}.$

Let $A = \{10\}.$ Find $Y ^{-1} (A)$ and using it

find $P(Y\in A).$

SOLUTION:

Here $Y^{-1}(A) = \{2,4,6\}.$ So $P(Y=10) = P(\{2,4,6\}) = \frac 16+\frac 16+\frac 16 = \frac 12.$

■

In each of these examples we had a random variable that

took only two values $10$ and $-20.$ Which random variable do

you think is more profitable for you, $X$ or $Y$? Well, both are actually the

same so far as profit goes. Understand this carefully: $X$ and $Y$

are completely different as functions (their

domains are also different), but in terms of the "behaviour of the

output" of the functions they are identical. This "behaviour of the output" is

called the distribution of the random variable. It is the

distribution which we care about mostly in real applications. So

we often start a discussion as

Let $X$ be a random variable taking values $10$

and $-20$ each with probability $\frac 12.$

We understand implicitly that there is some random experiment (say

the coin toss experiment or the die roll experiment or something

similar) and some function from its sample space

to ${\mathbb R}$ such that the distribution is as

specified. In this

course, we shall often omit the sample space or

the function.

How do we specify the distribution of a random variable? Do we make a list of all the subsets of ${\mathbb R}$, and label them with

their probabilities? That would be insane, because there are uncountably infinitely many such subsets.

It turns out that specifying the probabilities of intervals like $(-\infty, a]$ is enough.

This is what we discuss next.

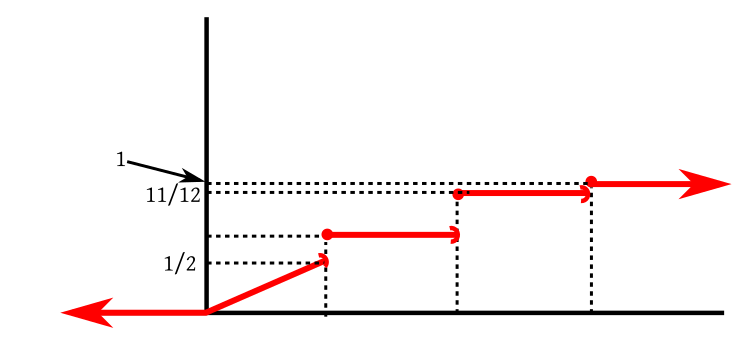

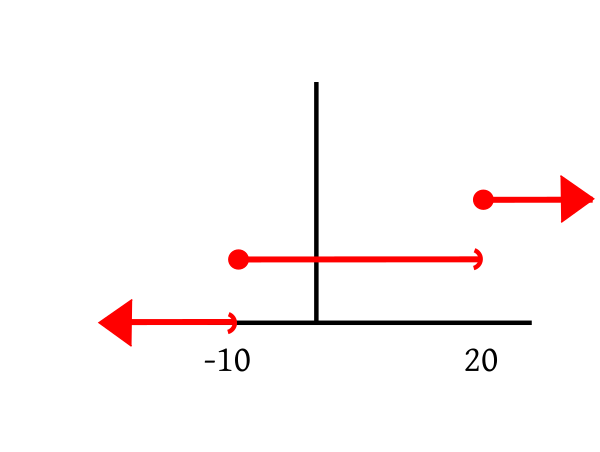

EXAMPLE 4: Consider the gambling game that tosses a coin, and has payoffs $-10$ for head, and

$20$ for tail. Let $X$ denote the payoff. What is its CDF?

SOLUTION:

Here $X$ takes only two values $-10$ and 20, each with probability $\frac 12.$

So $F(a) = P(X\leq a) = 0$ whenever $a<-10.$

But $F(-10)=P(X\leq -10) = \frac 12.$ Indeed, as long as $a\in[-10,20)$ we have $F(a) = \frac 12.$

At $a=20,$ we have $F(a) = 1.$ In fact, $\forall a\geq 20~~F(a) = 1.$ So the graph looks like this:

■

The following properties of a CDF are more or less obvious.

Shall show

$$

\forall \epsilon>0 ~~ \exists M \in{\mathbb R} ~~ \forall x < M~~ |F(x)-0| < \epsilon.

$$

(Actually we may drop the absolute value sign around $F(x)$

since it is anyway $\geq 0$).

Take any $\epsilon>0.$

Let $A_n$ be the event that $\{X \leq -n\}$

for $n\in{\mathbb N}.$ Then $F(-n) = P(A_n).$

Clearly, $A_1\supseteq A_2\supseteq A_3\supseteq\cdots$

and $\cap A_n=\phi.$

So $P(A_n)\rightarrow 0,$ i.e., $F(-n)\rightarrow 0.$

So $N\in{\mathbb N} ~~F(-N)<\epsilon.$

Choose $M = -N.$

Take any $x < M.$

Then $0\leq F(x) \leq F(M)<\epsilon,$ since $F(\cdot)$ is nondecreasing.

So $|F(x)-0| < \epsilon,$ as required.

Shall show

$$

\forall \epsilon>0 ~~ \exists M \in{\mathbb R} ~~ \forall x > M~~ |F(x)-1| < \epsilon.

$$

(Actually we may drop the absolute value sign

around $|F(x)-1|$ is $1-F(x)$,

since $F(x)\leq 1,$ anyway.)

Take any $\epsilon>0.$

Let $A_n$ be the event that $\{X \leq n\}$

for $n\in{\mathbb N}.$ Then $P(A_n)=F(n).$

Clearly, $A_1\subseteq A_2\subseteq A_3\subseteq\cdots$

and $\cup A_n=\Omega.$

So $P(A_n)\rightarrow 1,$ i.e., $F(n)\rightarrow1.$

So $N\in{\mathbb N} ~~|F(N)-1|<\epsilon.$

Choose $M = N.$

Take any $x > M.$

Then $0\leq 1-F(x) \leq 1-F(M) <\epsilon,$ since $F(\cdot)$ is nondecreasing.

So $|F(x)-1| < \epsilon,$ as required.

Shall show:

$$

\forall a\in{\mathbb R}~~\forall \epsilon>0~~\exists \delta>0~~ \forall

x\in (a,a+\delta)~~|F(x)-F(a)| < \epsilon.

$$

Take any $a\in{\mathbb R}$ and any $\epsilon>0.$

Let $A_n$ be the event that $\left\{X\leq a+\frac 1n\right\}$ for $n\in{\mathbb N}.$

Also let $A$ be the event that $\{X\leq a\}.$

Then $A_1\supseteq A_2\supseteq\cdots$ and $\cap A_n = A.$

So $P(A_n)\rightarrow P(A)$ and hence $F\left(a+\frac 1n\right)\rightarrow F(a).$

Hence $\exists N\in{\mathbb N} ~~ |F\left(a+\frac 1N\right)-F(a)|<\epsilon.$

Choose $\delta = \frac 1N>0.$

Take any $x\in (a,a+\delta).$

Since $F(\cdot)$ is nondecreasing, hence $F(a)\leq F(x)

\leq F(a+\delta) < F(a)+ \epsilon.$

So $|F(a+x)-F(a)|<\epsilon,$ as required.

[QED]

A rather nontrivial theorem is that the converse is also

true. This converse is called the fundamental theorem of

probability.

Proof:Too technical for this course.[QED]

Proof:

Let $F:{\mathbb R}\rightarrow{\mathbb R}$ be nondecreasing and bounded from above.

Take any $a\in {\mathbb R}.$

We shall show that $\lim_{x\rightarrow a-} F(x)$ exists as a finite

number, i.e.,

$$

\exists\ell\in{\mathbb R}~~\forall \epsilon>0~~\exists \delta>0~~\forall x\in(a-\delta,a)~~|F(x)-\ell|\leq\epsilon.

$$

Consider the set $A=\{F(x)~:~x < a\}.$ Then $A\neq\phi$

and bounded from above (by $F(a)$).

So $\sup(A)\in{\mathbb R}.$

Choose $\ell = \sup(A).$

Take any $\epsilon>0.$

Then $\exists y < a~~F(y) > \ell-\epsilon.$

Choose $\delta = a-y > 0.$

Take any $x\in(a-\delta,a) = (y,a).$

Then $F(y)\leq F(x) \leq \ell,$ or, in other words, $\ell-\epsilon\leq F(x)\leq \ell.$

So $|F(x)-\ell|\leq \epsilon,$ as required.

[QED]

Proof:

Take any $a\in{\mathbb R}.$

Let $A = \{X < a\}$ and let $A_n

= \left\{X \leq a-\frac 1n\right\}$ for $n\in{\mathbb N}.$

Then $A_n\nearrow A.$

Hence $P(A_n)\rightarrow P(A).$

So $F\left(a-\frac 1n\right)\rightarrow P(A).$

But $F\left(a-\frac 1n\right)\rightarrow F(a-),$ since $F(a-)$ exists.

Hence $P(X < a) = F(a-),$ as required.

[QED]

Depending on the distribution, a random variable may be of 3

types:

Discrete: These random variables take only countably

many (finite/infinitely many) values.

Continuous: If a random variable takes values in some

set $S$ such that $\forall a\in S~~P(X=a)=0,$ then we

call it a continuous random variable. Notice that

a continuous

random variable is not defined as a random variable that takes a

"continuous stretch of values". However, most continuous random

variables in practice do indeed take all values in an interval, e.g., height

of a randomly selected person.

Neither discrete nor continuous: These take

uncountably many values and for at least one value $a$ we

have $P(X=a)>0.$

The following theorem justifies the adjective "continuous" for a

random variable.

Proof:

Obvious from the last theorem.

[QED]

In this course we shall focus on discrete random variables only.

The distribution of a discrete random variable is completely

specified by the countable set of values it can take, and the

probability with which it takes each of those values. These two

specifications together are called the probability mass

function (PMF) of the rv.

Clearly, $\sum p_i = 1$ and $\forall i~~p_i\geq 0.$ A

consequence of the fundamental theorem of probability is that for

any countable set $\{x_1,x_2,...\}$ and for any

sequence $(p_i)_i,$ for which $\forall i~~p_i\geq 0$

and $\sum p_i=1,$ there is a (discrete) random variable of

which the PMF is $p(x)$ given above.

The CDF of a discrete random variable is a step function like the one we saw in our example.

$P(X=1) = P(X\leq 1)-P(X< 1).$

Now $\{X < 1\} = \lim_n \left\{X\leq 1-\frac 1n\right\}.$ Since this is an increasing limit, hence by continuity of

probability, we have $P(X<1) = \lim_n P\left(X\leq 1-\frac 1n\right) = \lim_n F\left(1-\frac 1n\right) = F(1-).$

Hence $P(X=1) = F(1)-F(1-).$

(b) $X$ can take values $0,1,...,n$. We have

$$P(X=k) = \binom{n}{k} \left(\frac 35\right)^k \left(\frac 25\right)^{n-k}$$ for $k=0,1,...,n$.

The PMF is zero otherwise.

(a) Here $n$ ca be at most 10. For $k=0,...,6$ we have

$$P(X=k) = \frac{\binom{6}{k}\binom{4}{n-k}}{\binom{10}{k}}. $$

Here we have the understanding that $\binom{n}{r} = 0$ if $r\not\in\{0,1,...,n\}$.

Clearly $X$ can take values in $\{1,2,...,12\}$.

So if $k\not\in\{1,2,...,12\}$, then $P(X=k) = 0$.

Now let $k\in\{1,2,...,12\}$.

Let the first number be $X_1$ and the second be $X_2$

Then $P(X\leq k) = P(X_1\leq k \& X_2\leq k) = P(X_1\leq k)P(X_2\leq k) = \left(\frac{k}{12}\right)^2$.

Actually this formula also holds for $k=0$.

So for $k\in\{1,2,...,12\}$ we have

$$P(X=k)= P(X\leq k)-P(X\leq k-1) = \frac{k^2-(k-1)^2}{144},$$

which is the required PMF.

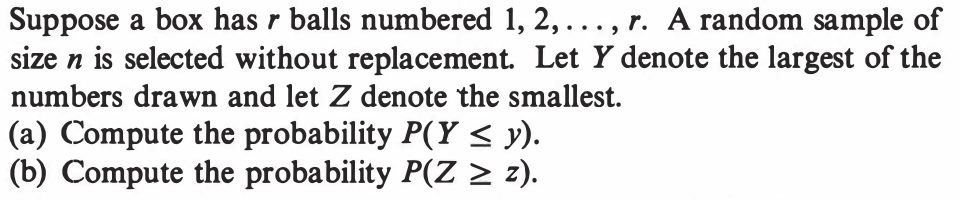

(a) Of course we assume that $n\leq r$.

Then $P(Y\leq y) = 0$ if $y < 1$ and also

$P(Y\leq y) = 1$ if $y\geq r$.

Let $y\in [1,r)$. Then $\{Y\leq y\}$ means all the balls are from $\{1,...,[y]\}$.

This has probability $\frac{\binom{[y]}{n}}{\binom{r}{n}}$.

(b) Similar.

First notice that since $F(x)$ is a continuous function, hence for any given $a\in{\mathbb R}$ we must have $P(X=a) = 0$.

So $P(X\geq 0.01) = P(X > 0.01) = 1-F(0.01) = e^{-\lambda/100}$.

So we get $e^{-\lambda/100}=\frac 12$ or $\lambda=100\log 2$.

Again, $P(X\geq t) = e^{-\lambda t}$.

So we need $e^{-\lambda t} = 0.9$. Hence $t = -\frac{\log 0.9}{\lambda} = -\frac{\log 0.9}{100\log 2}$.

This is actually positive, since $\log 0.9 < 0$.

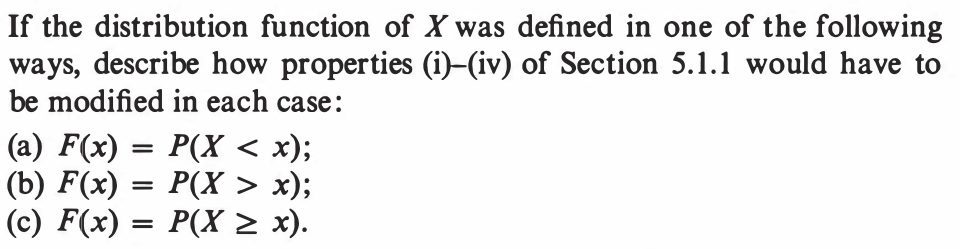

(a) (i), (ii), (iii) No modification. (iv) $F(x-) = F(x)$ for all $x$.

(b) (i) No modification. (ii) nonincreasing. (iii) $F(-\infty) = 1$ and $F(\infty) = 0$. (iv) No modification.

(c) (i) No modification. (ii) nonincreasing. (iii) $F(-\infty) = 1$ and $F(\infty) = 0$. (iv) $F(x-) = F(x)$ for all $x$.

Don't let the notation $X ^{-1}$ make you think that $X:\Omega\rightarrow{\mathbb R}$ has to be

invertible. For any $f:A\rightarrow B$ we can define $f ^{-1}:\pow(B)\rightarrow\pow(A)$ as follows (here $\pow$ denotes

power set, i.e., the set of all subsets):

for $V\in\pow(B)$ we define $f ^{-1}(V)=\{a\in A~:~f(a)\in V\}$.

Don't let the notation $X ^{-1}$ make you think that $X:\Omega\rightarrow{\mathbb R}$ has to be

invertible. For any $f:A\rightarrow B$ we can define $f ^{-1}:\pow(B)\rightarrow\pow(A)$ as follows (here $\pow$ denotes

power set, i.e., the set of all subsets):

for $V\in\pow(B)$ we define $f ^{-1}(V)=\{a\in A~:~f(a)\in V\}$.